Lightning Network Value Prop

Who's using it, why, and the journey along the tech adoption curve

After writing last post on the Lightning Network, I wanted to know who is using it today, and why. I was surprised to find a broad ecosystem of users, including many of the prominent crypto companies.

That said, as a general payments technology, it still has a long way to go. Just like other new entrants, it doesn't solve every need for every person, but it does solve hard problems for an important group of people, and that group will grow over time.

In this post, I do a bottoms-up analysis of who is using Lightning, what problems it solves for them, and how it fits into the context of other payment technologies. Here's the plan:

Lightning adopters today

Criteria to decide which payment technologies to use

Public vs private payment infrastructure

Lightning value proposition

Lightning limitations and risks

Lightning Adopters Today

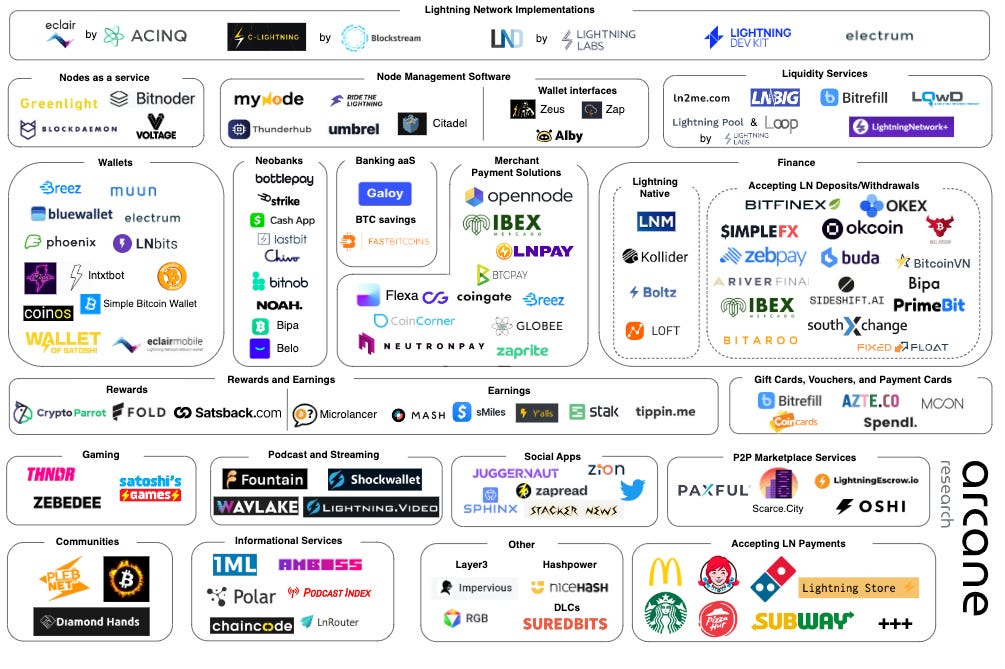

Let's start from the ground up with a look at the ecosystem and any patterns among their users. Although a year old, this map below has many of the active players today.

Within that ecosystem, there a few categories driving much of the end-user activity:

Crypto Exchange or Bank: Bitfinex, Kraken, Xapo, Rain, Binance

Digital content and social media: Nostr, Twitter, Zion, Fountain, StackerNews

Gaming: Square Enix, Fumb Games, THNDR, ZBD

Merchants: PizzaHut (in El Salvador), Lightning Store, McDonalds

Crypto wallets: Phoenix, Wallet of Satoshi, Breez

And within this group, the users seem to have one or a few of these common traits:

Active cryptocurrency users

Sending small consumer payments

Threatened by fragile financial system (e.g. countries with inflation)

Want protection from getting de-platformed (e.g. Nostr, Zion)

Trying new models for content creators (e.g. Fountain)

Criteria to Decide Which Payment Technologies to Use

I have nine payment apps on my phone.

Innovations in payments come fast and often. There's Visa, Mastercard, ACH, PayPal, Venmo, Zelle, Apple Pay, Starbucks App, Cash App, WorldPay, UnionPay, FEDNow, Stripe, Amazon Pay, every bank app.

Companies make decisions on which payment gateways to integrate for a variety of reasons. The reasons typically include credit card transaction fees, international transaction fees, currency conversion fees, countries supported, currencies supported, and recurring payment support.

On certain dimensions, Lightning is a strong alternative to existing options.

Private vs Public payment infrastructure

The reason Lightning is a strong alternative is because it's built on the world's first public payment infrastructure: Bitcoin. "Public" in the sense of not owned by any one company or government. It works without intermediaries, unlike the payment technologies today that rely on a concoction of banks, tech companies, and service providers. These private companies all insert their business model into the payment flow, often taking a cut and increasing costs to users.

The best explanation of this is the congressional testimony below from Peter Van Valkenburgh, Director of Research at Coin Center.

As Peter says, to send money over the internet today, you need to open a bank account. So does your counterpart. You need to find a common payment rail, either through your bank or through connecting to an external application like Venmo. To pay a merchant you might open a Visa credit card and rely on even more private companies to transfer the value. All these steps include gatekeepers and fees.

On Bitcoin, anyone can open an account for free to receive value. There's no restrictions on race, gender, location, or creditworthiness. As he said, "bitcoin is the first globally accessible money."

So what does this mean for businesses and consumers?

Lightning Value Proposition

Lightning outperforms other payment technology in its fees, global support, and interoperability. Here's what that means for businesses today.

Reduce fees and offer better prices

According to the WooCommerce chart, credit card fees are usually 2.9% + $0.30, international transactions add another 1-1.5%, and currency conversations add another 1-4%.

There's also dispute fees and the risk of chargebacks.

Lightning fees are fractions of a penny, essentially negligible. And it's inherently global so there are no international fees or conversion fees. Businesses can choose to pass along the savings to their customers and offer lower prices than their competitors still paying that 2.9+% in fees.

Easy onboarding for global customer base

As you can see in the chart above, not every provider is supported globally. This means merchants will lose customers if they don't offer a service supported in the customer's region.

Bitcoin is the first globally accessible money. By using Lightning, a provider is immediately tapping into a global audience of everyone who simply has an internet connection.

Faster cross-border payments

Rain is one of the largest crypto exchanges in the MENA region. I'll let their press release explain this one:

"[Lightning] will enable faster and cheaper remittances, allowing people to send and receive money across borders in a matter of seconds, rather than days or even weeks. Any other financial application, in any country, that supports Lightning Network can now speak to Rain users. For example, a Rain user can for the first time send Bitcoin instantaneously to a CashApp user in the US."

Improve robustness and reduce dependence on fragile financial system

Peter, in the video above, explains that reducing reliance on the private institutions intermediating our payment networks is important because these institutions are getting fewer, bigger, and causing harsher catastrophes when they fail.

We're living in a time with increasing signals of risk that are worth hedging against. In the US and abroad, we've had had bank collapses like SVB and Credit Suisse, inflation at historic highs, debt at historic highs, and a likely recession approaching.

It seems prudent to consider a parallel system to stay online in case surprising events happen like when SVB became insolvent and halted withdrawals without warning only a few months ago.

Attract like-minded customers

Bitcoiners are a strong cultural group that likes to use Bitcoin technology. Offering Lightning payments will attract this group to you.

Lightning limitations and risks

All that said, currently, there are significant limitations and risks.

It's technically challenging to operate. Lyn Alden explains that "your node has to be on all of the time, you tie up a lot of capital, and it can be tricky to balance your liquidity." Service providers are sprouting up to help, but even they are still learning how best to provide enterprise-grade reliability and stability. Much of the operational processes are still manual and time consuming. On top of that, the network itself is rapidly evolving and requires effort to keep up.

It cannot support large size transactions. From my research, the method to send large payments on Lightning was able to send 0.6 bitcoin a year ago. The limit is likely higher today, which is enough for most consumer payments, but less than many large-size transactions.

Many people do not want to transact in bitcoin. Many view bitcoin as a store of value, and not something to spend. Also, transacting in bitcoin is a taxable event in many countries.

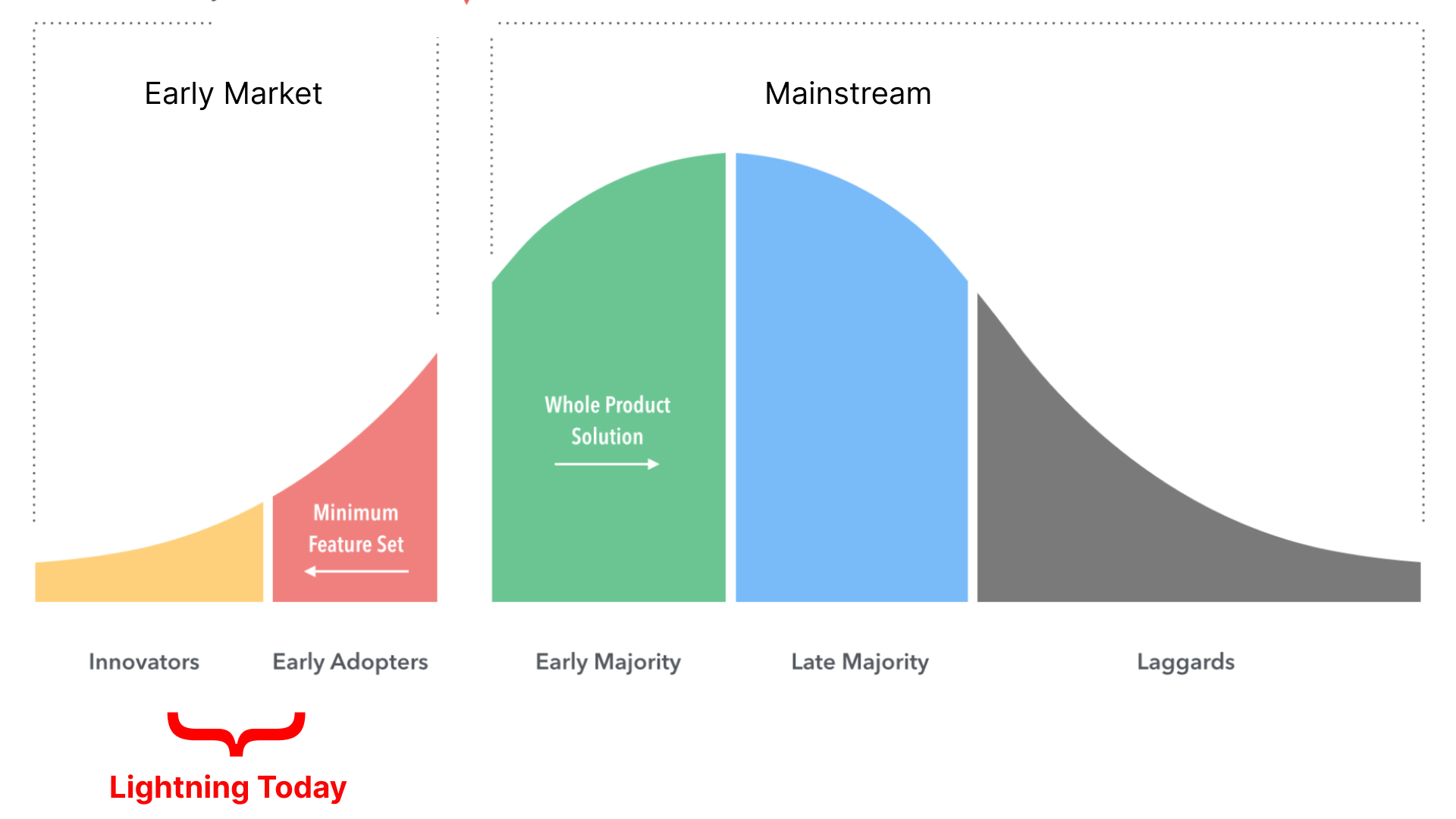

Step by Step

Lightning is in the early adopter phase of its tech adoption curve. A niche group is willing to accept the challenges because the reward is high for them. With more tech improvements, service providers, and integrations, it will become more valuable to more groups and outperform its competitors along more dimensions.

I'll conclude the same as last post, with the mic drop from Lightning Labs CEO Elizabeth Stark:

“If I were Visa, I’d be scared, because there are a lot of people out there that have mobile phones, but now don’t need to tap into the traditional system, and then the merchants don’t need to pay the 3% fee plus 30 cents [for a transaction]. You can have fees that are dramatically lower than the legacy system.”